1. The global baseline: ISSB as your starting point

The International Sustainability Standards Board (ISSB) has created a global “baseline” for sustainability disclosures focused on information that is material for investors and lenders.

IFRS S1 sets general requirements for disclosure of sustainability‑related financial information across all topics.

IFRS S2 sets specific requirements for climate‑related disclosures, built on the Task Force on Climate‑related Financial Disclosures (TCFD) architecture.

Together, S1 and S2 are designed to produce robust, comparable and verifiable information on sustainability‑related risks and opportunities that could affect cash flows, access to finance or cost of capital. Even where your primary obligations are under UK or EU law, treating ISSB as the spine of your reporting architecture makes it much easier to serve multiple regulators and capital providers from a single data model.

2. UK Sustainability Reporting Standards (UK SRS) in 2026

For UK‑headquartered or UK‑listed groups, the UK Sustainability Reporting Standards (UK SRS) are the key development in 2026.

What UK SRS S1 and S2 require

The UK government has endorsed ISSB’s IFRS S1 and S2 and issued them as UK SRS S1 and UK SRS S2, with minor jurisdictional tailoring.

UK SRS S1 sets out the general framework for sustainability‑related financial disclosures, covering any sustainability matter that could reasonably affect a company’s cash flow, access to finance or cost of capital.

UK SRS S2 focuses on climate‑related risks and opportunities, and requires disclosure of governance, strategy, risk management, metrics and targets, including Scope 1, 2 and 3 greenhouse gas emissions.

These standards are intended to be used together with the financial statements, so investors can understand how sustainability factors interact with performance and position.

Who is in scope and when

The government has indicated that UK SRS will apply initially to listed and “economically significant” entities for accounting periods starting on or after 1 January 2026, with the FCA consulting on detailed listing‑rule changes during 2026. Even if you are not formally in scope on day one, banks, investors and large customers will increasingly expect data structured in line with UK SRS and ISSB.

What this means for sustainability, finance and risk teams

Sustainability and finance must work together to identify material sustainability‑related risks and opportunities using the same rigour as other principal risks.

Data systems must connect operational data (emissions, energy, supply chain) with financial ledgers to support auditable disclosures and future assurance requirements.

Scenario analysis, transition plans and carbon pricing assumptions need to be embedded into planning and risk management, not left in standalone ESG decks.

Kick‑start UK SRS adoption with templates

With a bsustainable today membership, your team can download UK SRS‑aligned disclosure planners, KPI inventories and template board papers that help you translate the text of S1 and S2 into practical, finance‑ready outputs. This shortens the journey from “understanding the standards” to having your first working drafts for 2026 periods.

3. EU CSRD, ESRS and double materiality

If your group has substantial operations in the EU, is EU‑listed, or meets CSRD thresholds via EU subsidiaries, the Corporate Sustainability Reporting Directive (CSRD) and European Sustainability Reporting Standards (ESRS) will drive your 2026–27 reporting.

Double materiality as a legal requirement

CSRD makes a structured double materiality assessment the mandatory starting point for all in‑scope companies.

Impact materiality considers how your business affects the environment and society.

Financial materiality considers how sustainability‑related risks and opportunities affect your enterprise value.

The ESRS 1 General Requirements standard and subsequent implementation guidance clarify how companies should run this assessment, emphasising strategic judgement over box‑ticking. Double materiality acts as a filter to determine which ESRS topical standards (for climate, pollution, workers, business conduct and more) you must actually disclose.

Phasing and revised ESRS

Revised ESRS and implementation guidance submitted by EFRAG in late 2025 are expected to be adopted in summer 2026, with different “waves” of companies stepping into full reporting over several years. Large companies already reporting under the old Non‑Financial Reporting Directive continue under existing ESRS until they switch to the updated set, while a second wave of large EU companies reports later in the decade.

Synergies with GRI and voluntary reporting

For companies already using the GRI Standards, CSRD offers significant synergies, because ESRS impact materiality is explicitly aligned with the GRI 3 Material Topics standard. To reach full CSRD compliance, you mainly need to add the financial materiality lens and meet the specific ESRS datapoint requirements.

bsustainable today support for CSRD and ESRS

By choosing a bsustainable today membership, your sustainability, finance and risk teams can download practical templates for double materiality mapping, stakeholder mapping, ESRS datapoint registers and disclosure planners. These resources are designed so you can move from “we should start a CSRD project” to “we have a structured assessment and a draft ESRS roadmap” in days, not months.

4. EU Taxonomy, EU ETS and climate pricing

CSRD does not operate in isolation. It sits alongside the EU Taxonomy for sustainable activities and the EU Emissions Trading System (EU ETS), both central to how European regulators and investors view transition risk.

EU Taxonomy and sustainable activities

The EU Platform on Sustainable Finance advises the European Commission on updates to Taxonomy technical screening criteria and on streamlining the wider sustainable finance framework. As of 2026, the Platform is focused on:

Reviewing and updating screening criteria for climate and other environmental objectives.

Making Taxonomy application more workable for SMEs and improving monitoring of capital flows into sustainable investments.

Under CSRD, in‑scope companies must disclose the share of their turnover, capex and opex associated with Taxonomy‑eligible and Taxonomy‑aligned activities. That requires robust project‑level and asset‑level data linked to financial systems.

EU ETS and carbon risk

The EU ETS continues to expand as the EU’s main carbon pricing mechanism, covering power, industry and additional sectors over time. For many companies, verified emissions, allowances and carbon costs under EU ETS now form critical inputs into risk modelling, scenario analysis and valuation, which must be disclosed under ESRS climate standards, UK SRS S2 and ISSB.

For project finance and capital‑intensive sectors, this turns EU ETS into a financial framework as much as an environmental one: assumptions about future carbon prices feed directly into NPV, impairment tests and credit decisions.

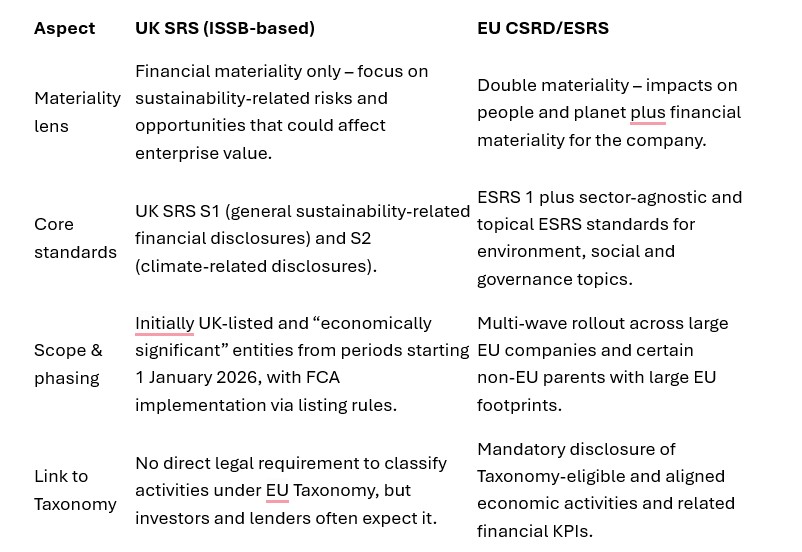

5. UK vs EU disclosure expectations: key differences

If you operate across both the UK and EU, you need to serve two subtly different but compatible

The practical solution is to build a common core dataset aligned to ISSB/UK SRS, then apply a double‑materiality overlay and additional datapoints for CSRD/ESRS.

6. Sustainable finance: green bonds, SLLs and project finance

Sustainability frameworks now shape not just reporting but also how you structure and price your financing.

EU green bond standard

The EU green bond standard (EuGB) provides a regulated label for bonds whose proceeds are allocated to EU Taxonomy‑aligned green activities.

Issuers must commit to Taxonomy‑aligned use of proceeds, provide detailed allocation and impact reporting, and use registered external reviewers.

From June 2026, external reviewers of EuGBs must be authorised and supervised by ESMA, raising the bar on quality and consistency.

This means treasury and sustainability teams must be able to map projects against Taxonomy criteria and generate credible, verified impact data.

Sustainability‑linked loans and sustainability‑linked loan financing bonds

Sustainability‑linked loans (SLLs) tie loan pricing to the borrower’s performance against agreed sustainability KPIs and targets.

ICMA and the Loan Market Association issued Guidelines for Sustainability‑Linked Loans financing Bonds (SLLBs), recommending that portfolios be built on the existing Sustainability‑Linked Loan Principles.sustainablefutures.

SLLBs are bonds whose proceeds finance a portfolio of SLLs, combining “use of proceeds” structures with performance‑based KPIs at loan level.

In practice, lenders and investors now expect:

KPIs that are aligned with recognised frameworks (e.g. SBTi‑aligned emissions reductions, ESRS/ISSB metrics, Taxonomy‑linked performance).

Transparent methodologies, baselines and verification, so margin ratchets reward genuine improvements rather than soft targets.

For project finance, this allows you to link funding costs to lifecycle performance against emissions, resilience and other ESG metrics defined in line with CSRD, UK SRS and ISSB.

Use templates to align your financing structures

bsustainable today membership includes example KPI libraries, SLL/SLLB term‑sheet checklists and Taxonomy‑mapping tools that help treasury and sustainability teams design credible, framework‑aligned financing structures faster. This gives you a head start when negotiating with lenders and investors.

7. Turning multiple frameworks into one roadmap

With so many overlapping frameworks, the core challenge for teams is integration, not awareness.

Build a single sustainability data foundation

Map your entities and value chain against UK SRS, CSRD/ESRS, EU Taxonomy, EU ETS and ISSB to understand which obligations and expectations apply.

Design a unified data model that links operational, emissions and financial data so you can report once and use many times – for regulators, banks, investors and rating agencies.

Align governance, risk and capital allocation

Update risk frameworks so sustainability‑related risks and opportunities are assessed alongside credit, market and operational risk, in line with ISSB, UK SRS and ESRS expectations.

Ensure board and committee mandates explicitly cover oversight of sustainability‑related financial disclosures and Taxonomy‑aligned capital allocation.

Connect frameworks to the cost of capital

For green bonds and EuGBs, build Taxonomy and ESRS metrics into eligibility criteria and reporting plans from the term‑sheet stage.

For SLLs and SLLBs, base KPIs on your UK SRS/ISSB metrics and CSRD transition plan, so that pricing ratchets are strategically meaningful.

Prepare for assurance and scrutiny

Anticipate a move from limited to reasonable assurance over key metrics, and strengthen controls and audit trails accordingly.

Engage early with investors, lenders and rating agencies, using ISSB‑, UK SRS‑ and CSRD‑aligned data to demonstrate resilience and value creation.

How bsustainable today membership helps you execute

For most teams, the hardest part is not understanding the rules, but turning them into concrete checklists, registers and board‑ready packs. By choosing a bsustainable today membership, your sustainability, finance and risk teams can immediately download practical templates that kick‑start adoption of UK SRS, CSRD/ESRS, ISSB and EU Taxonomy – from double‑materiality matrices and framework‑mapping spreadsheets through to draft policy outlines and board briefing decks. These resources are designed so you can move from “we should do this” to “here is the first working version” in days, not months.

Kick‑start your framework adoption

Ready to move from reading about CSRD, UK SRS, ISSB and EU Taxonomy to actually implementing them? With a bsustainable today membership, you get instant access to downloadable templates, checklists and example disclosures that align with the main 2026 frameworks. Choose your membership package, download the tools you need, and start building a coherent sustainability framework for your business today.

8. So which frameworks apply to you in 2026?

While the exact mix depends on your footprint and financing strategy, most mid‑to‑large businesses will face the following reality in 2026:

UK‑focused businesses: UK SRS S1 and S2 as the primary standards, underpinned by ISSB, plus existing climate and energy reporting requirements such as SECR.

EU‑exposed businesses: CSRD and ESRS, a mandatory double materiality assessment, EU Taxonomy disclosures and growing interactions with EU ETS.

Global and multi‑listed groups: ISSB as the global baseline, with jurisdictional overlays for UK SRS, CSRD/ESRS and other emerging regimes.

The real decision is whether to treat these frameworks purely as a compliance burden, or to use them as a lever to reduce financing costs, strengthen resilience and differentiate with stakeholders. If you are ready to move from understanding the frameworks to actually embedding them, bsustainable today membership gives your teams the templates and tools to start that journey immediately.